TLDR

THORChain relies on active arbitrage to function.

Arbitrage is currently inefficient and costs users through sub-optimal swap execution.

Base Layer liquidity for major pairs cannot currently scale due to THORFi overhang.

This means Base Layer TVL growth is constrained unless RUNE price rises.

Rujira can use the end-block scheduler to deploy App Layer liquidity into Base Layer pools.

This introduces a new liquidity model for THORChain and enables more capital-efficient market making.

Base Layer pools can track market prices more closely and quote more competitively.

Combined with rapid swaps, this can also improve settlement speed.

We estimate monthly arbitrage volumes around ~$800m on THORChain, with roughly ~$3m in arbitrage profits.

A share of that can be internalized by Rujira while improving execution quality for THORChain users.

Context

THORChain volumes are driven by two broad event types:

Organic usage, where users swap assets through frontends and integrators.

Pure arbitrage, where pool prices lag broader market prices and get rebalanced.

In both cases, dislocations between pool prices and external prices create arbitrage opportunities. Looking at Trade Asset volume share, arbitrage appears to represent roughly 60% of THORChain volume.

Every organic swap in Base Layer Continuous Liquidity Pools pushes pool pricing away from equilibrium, and arbitrageurs are needed to rebalance. The larger the swap relative to pool depth, the larger the deviation under XYK dynamics.

Large market moves also create pool-to-market dislocations that attract arbitrage. Larger Base Layer TVL supports larger rebalancing flow, so healthy TVL is directly tied to throughput and competitiveness.

TVL in Base Layer pools can no longer scale

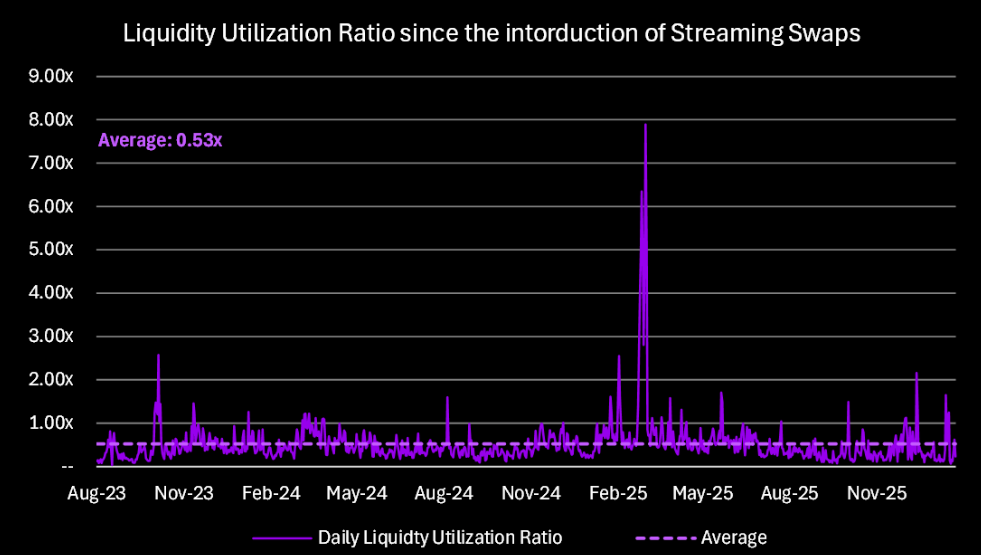

THORChain improved capital efficiency by introducing streaming swaps. Large swaps are split across multiple blocks, trading execution speed for better pricing while relying on arbitrageurs to rebalance between each sub-swap.

The Daily Liquidity Utilization ratio (Daily Volume / End-of-day TVL) increased from an average of 0.15x pre-streaming swaps (April 2021 to August 2023) to around 0.53x post-streaming swaps (September 2023 to January 2026).

This improvement led some to assume TVL no longer matters for volume. The data suggests the opposite.

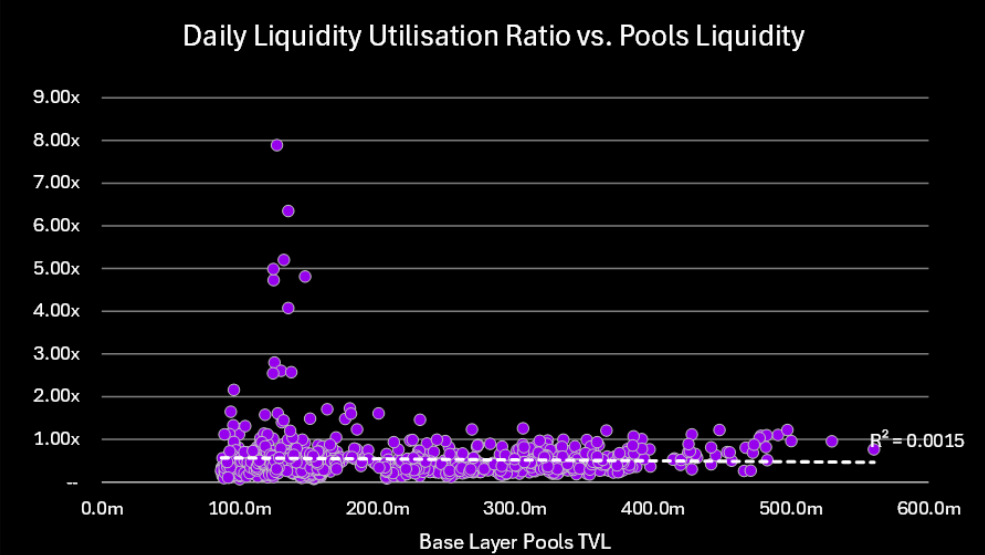

The chart below compares Daily Liquidity Utilization ratio against Base Layer pool liquidity. If volume were independent of TVL, utilization would fall as TVL rises. Instead, utilization remains broadly consistent across time and across TVL levels, from above $500m down to below $100m.

In practice, volume scales close to linearly with TVL: higher TVL enables higher volume and higher protocol revenue.

Due to THORFi overhang, THORChain now faces a structural constraint: Base Layer TVL for major pairs such as BTC, ETH, USDC, and USDT cannot be increased through deposits. In those pools, TVL growth depends heavily on RUNE price, which limits growth and makes arbitrage efficiency even more important.

Arbitrages are currently sub-optimal

THORChain depends on arbitrage, but current arbitrage quality is uneven. External arbitrageurs often allow meaningful price drift before rebalancing. Users can therefore execute at prices materially worse than broader market prices, especially when streamed swaps start.

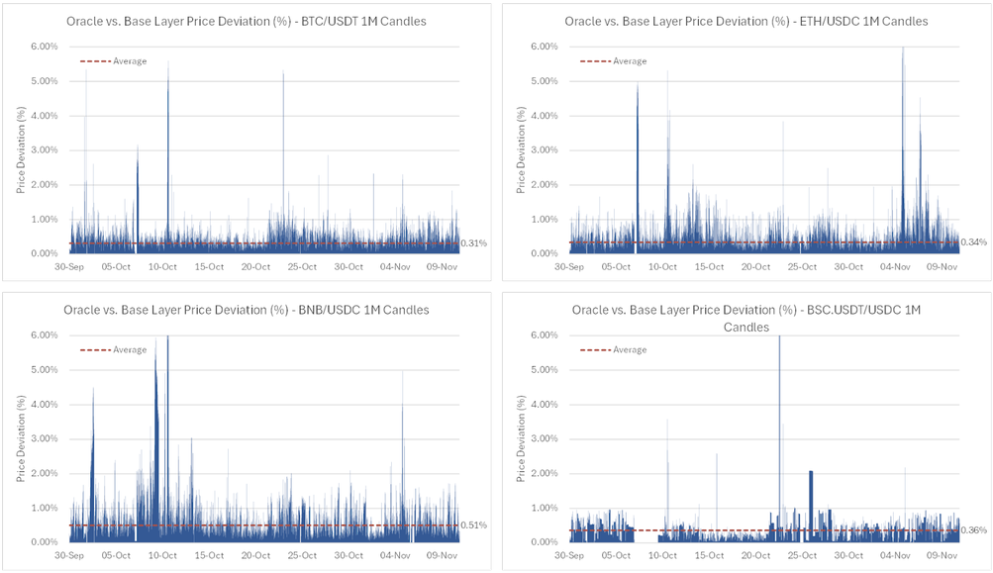

This is visible even on stable-to-stable pairs.

Our analysis shows average price deviation around 0.40%, with frequent spikes above that level. One likely factor is arbitrage loop latency and inventory movement between CEXs and onchain venues.

THORChain v3.12 introduced an onchain scheduler that allows App Layer contracts to schedule execution and gain deterministic timing at the start of end-block processing. That allows contracts to execute arbitrage and rebalance Base Layer pools with improved precision using App Layer liquidity.

This creates a path to:

Support Base Layer liquidity constrained by THORFi.

Use more capital-efficient concentrated liquidity strategies rather than pure XYK.

Add stablecoin- or BTC-paired liquidity (instead of only RUNE reflexive exposure).

Improve settlement speed for larger swaps when combined with rapid swaps.

Example

Imagine a large Base Layer swap buying BTC with USDC pushes BTC in the Base Layer pool 0.40% above the ask on the BTC/USDC RUJI Trade orderbook.

Assume:

App Layer AMM strategies (including CCL and future strategies) can quote meaningful size near current ask.

RUJI Trade AMM fee is 0.025% (2.5 bps).

Base Layer Secured Asset swap fee (

SecuredAssetSlipMinBps) is 10 bps per leg, so a two-leg route costs 0.20%.The VS target reserve fee is 0.10%.

That implies total arbitrage cost near 0.325%. So price deviation must be above 0.325% to trigger overlap between VS and App Layer quotes. At 0.40% deviation, approximately 0.075% remains as net arbitrage profit (on top of Base Layer liquidity fees).

Flow of funds:

VS bids for quantity X BTC at Base Layer pool price minus 32.5 bps.

Other App Layer AMM strategies quote quantity Y BTC at 40 bps below Base Layer price.

The scheduler matches overlapping quantity

MIN(X, Y)and captures spread plus AMM fees.VS borrows USDC from lending vaults and fills on the App Layer side.

VS injects a swap request to sell acquired BTC on the Base Layer at inflated price minus Base Layer liquidity fee.

On the next block, proceeds repay the USDC loan.

VS retains the remaining balance as profit.

Because matching happens block by block, this model reduces prolonged pool drift and should improve average execution prices for THORChain users.

As DCL strategies are added, the App Layer should be able to quote larger sizes close to oracle price, increasing overlap quality and keeping Base Layer pools closer to true market.

Looking into the data

Exact within-block price-impact attribution is difficult with current data granularity. But on 1-minute candles, deviations above 0.40% are frequent and deviations above 1% are not rare. A scheduler-driven model should bring prices back toward oracle more frequently.

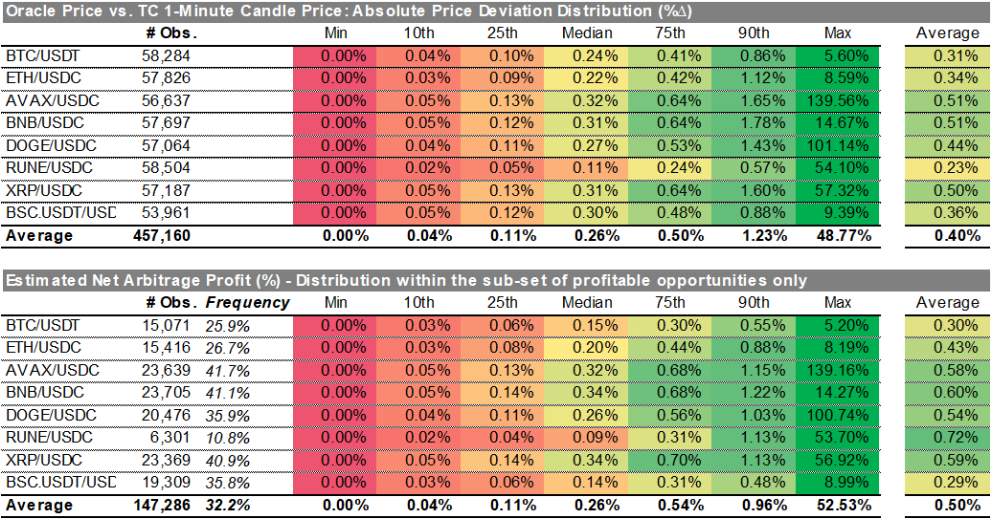

We analyzed 8 high-volume pairs using 1-minute candles from 30-Sep-2025 to 10-Nov-2025 (about 40 days, roughly 57k data points per pair), comparing THORChain Base Layer closes with Enshrined Oracle prices.

We then summarized absolute deviation and estimated net arbitrage profit by percentile. Profit assumptions include:

0.325% base cost from the example.

Plus 0.025% for DCL AMM fees.

Plus 5 bps spread for LP liquidity.

That implies a minimum profitable deviation near 0.40%.

Key observations:

Average deviation is around 0.40%, close to the modeled profitability threshold.

90th percentile deviation is around 1.23%, indicating a meaningful upper tail.

Deviation ranges are relatively consistent across pairs, generally around 0.3% to 0.5%.

Higher-volume pairs and major stables tend to sit toward the lower end, consistent with stronger arbitrage competition.

Quantifying the opportunity

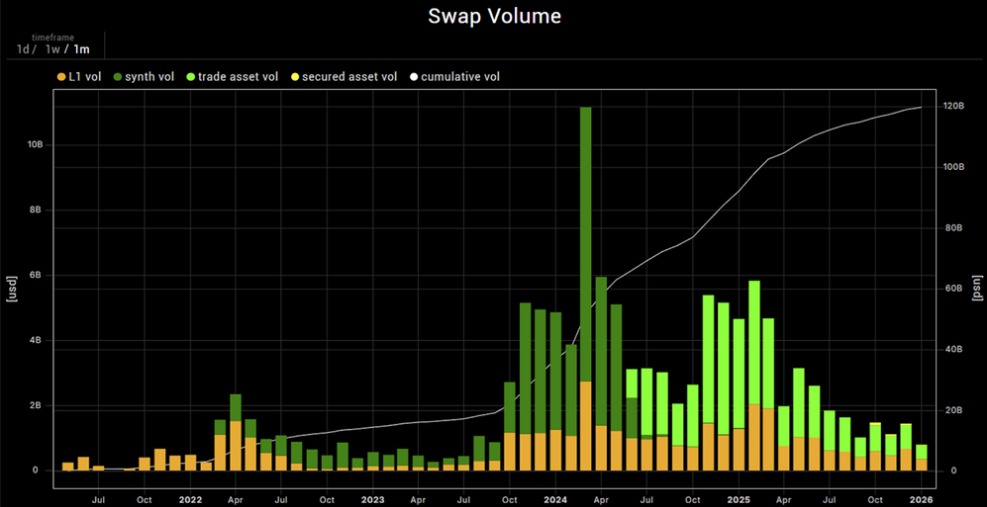

Using historical THORChain volume and Trade Asset share as a proxy for arbitrage-dominated flow, Trade Assets have represented around 60% of total volume over time.

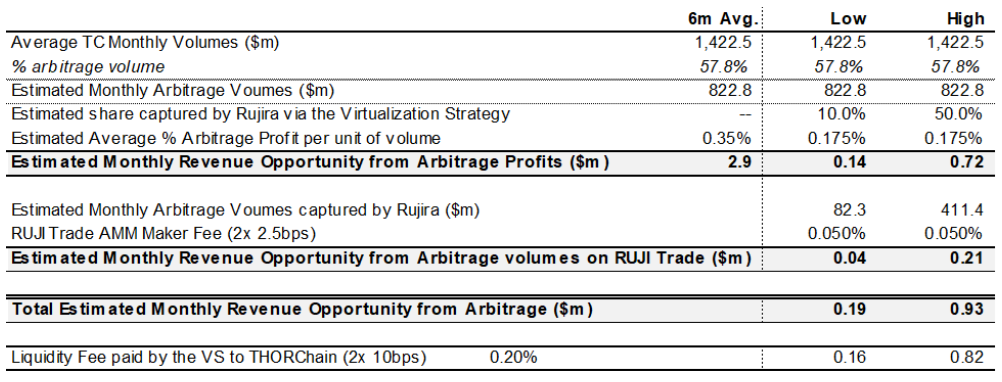

Over the last 6 months, THORChain volume has averaged around $1.4bn monthly, with estimated arbitrage volume near $0.8bn. At approximately 0.35% average arbitrage profit, that implies roughly $2.9m monthly arbitrage profit pool.

If Rujira internalizes part of this flow, it can execute arbitrage more consistently, reduce average deviation for users, and capture protocol-side value.

The practical share captured will depend on App Layer liquidity depth (AMM TVL and lending vault liquidity), as well as competition from external arbitrageurs with low-fee CEX access.

Illustrative outcomes in the current setup:

Rujira could capture meaningful monthly incremental revenue from arbitrage and AMM matching fees.

THORChain also accrues value through Base Layer liquidity fees charged during VS execution.

Disclaimer: These estimates are illustrative and assumption-driven. Actual outcomes may differ materially. Always do your own research.

A balancing act

There are several parameters to optimize for best results across pricing quality, throughput, and protocol revenue:

SecuredAssetSlipMinBpson THORChain Base Layer swaps.VS reserve fee settings and quote logic.

RUJI Trade AMM fee tier.

LP fee/spread configuration for concentrated liquidity strategies.

There is meaningful room to tune these over time and move toward a better equilibrium between execution quality and monetization.

Next steps

To execute this model, the core building blocks are:

Current VS version, already live, with quote capacity growing as lending liquidity grows.

Custom Concentrated Liquidity (CCL), already in testing/live paths for key pairs.

Scheduler-driven automatic arbitrage between liquidity sources on RUJI Trade.

Additional roadmap items:

Launch Dynamic Concentrated Liquidity (DCL) to keep quotes close to oracle and scale pure arbitrage participation.

Launch Average Down / Profit Up (ADPU) strategy for user-specific AEP tracking and adaptive inventory management.

Upgrade VS quote sizing logic to account for pending swap queue state more accurately.

Coordinate with Nine Realms on Base Layer quote API upgrades that reflect App Layer liquidity impact on settlement time.

Closing thoughts

Internalizing part of arbitrage flow through the Virtualization Strategy can create a meaningful revenue stream while improving user execution outcomes.

It gives THORChain a way to scale effective liquidity again with capital-efficient App Layer strategies, without relying purely on reflexive RUNE-driven pool growth.

This is a practical alignment between THORChain and Rujira: better pricing, faster settlement, stronger competitiveness, and shared upside from improved market structure.